This article will introduce you to the entire process of purchasing a new condominium in Singapore:

1. Financial Planning

2. House Hunting and Viewing

3. Paying the Deposit

4. Hiring a Lawyer

5. Signing the S&P Agreement

6. Paying Stamp Duty

7. Completing the Transaction

8. Waiting for the Condominium to Be Completed (Progressive Payment for Building Under Construction)

9. Property Inspection

1. Financial Planning

Private condominiums are the type of property in Singapore with the fewest restrictions on the eligibility of homebuyers. Whether you are a Singapore citizen, a permanent resident, or a foreigner, you can purchase them. You just need to plan your financial planning in advance before starting your home-buying journey.

If you plan to buy a property with a loan, you need to approach a bank in advance to obtain an IPA (In-Principle Approval). The bank will match a loan amount according to each individual's situation, which means the bank agrees in principle to provide the homebuyer with a certain amount of loan. The maximum Loan To Value (LTV) Ratio in Singapore is 75%. Calculate the upper limit of your home-buying budget based on the approved loan amount. Prepare at least 25% of the total purchase price as down payment. If you are buying the house in full, prepare the corresponding cash.

In addition to the property price itself, taxes, legal fees, and other expenses also need to be taken into account. Taxes mainly refer to stamp duty, including Buyer's Stamp Duty (BSD) and Additional Buyer's Stamp Duty (ABSD).

BSD - Buyer's Stamp Duty

BSD is a basic tax applicable when purchasing a property located in Singapore. BSD is computed based on the higher of the purchase price or the market value of the property, with a progressive tax rate applied, and the total tax payable is the sum of the taxes in each tier.

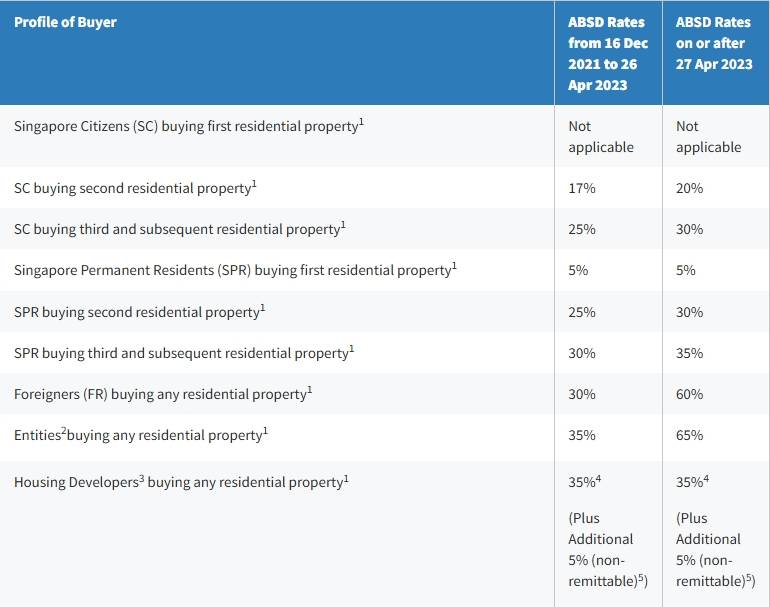

ABSD - Additional Buyer's Stamp Duty

Whether ABSD needs to be paid and the amount payable depends on factors such as the buyer’s residential status and the number of residential properties owned by the Buyer.

You also need to appoint a lawyer to assist you in reviewing and signing the Sales and Purchase (S&P) Agreement and Loan Contract , clarify the legal terms in the agreements, and ensure that the transaction process is legal and compliant. Legal fees may vary depending on the complexity of the transaction, and generally range from $2,000 to $5,000.

Comprehensively consider factors such as the down payment, monthly mortgage payment, and taxes, etc. Determine your home-buying budget accordingly. Then you can start looking for properties.

2. House Hunting and Viewing

Look for new condominium projects that fit your budget. You can search for properties through reputable real estate websites, such as the HouseBell platform, where all the property information is authentic and reliable. Alternatively, you can find a real estate agent to help you,which saves time and effort. When buying a new condominium in Singapore, the buyer does not need to pay the agent’s commission.

When looking for projects, its important to comprehensively consider factors such as location, transportation, environment, and surrounding supporting facilities (commerce, schools, medical care). Gather detailed information about the project, including the size of the community, internal facilities, building spacing, etc., as well as the developer's reputation and the quality of past projects.

Learn more details about the property, such as the unit layout, area, price, and delivery time. Arrange an on-site viewing, visit show flats, and carefully observe the interior decoration, layout, lighting, and ventilation of the house. At the same time, conduct on-site evaluations of the surrounding environment and facilities within the community.

3. Paying the Booking Fee

After selecting the property you like, you can pay 5% of the total purchase price as a booking fee to reserve the unit from the developer. After receiving the booking fee, the developer will issue an Option to Purchase (OTP), which will indicate important information such as the details, price, deposit, and payment method of the condominium. After obtaining the OTP, the buyer can approach the bank for loan matters and obtain a Letter of Offer (LO) issued by the bank as preliminary proof that the homebuyer is eligible to obtain a loan from that bank.

4. Hiring a Lawyer

After paying the booking fee, you need to appoint a lawyer as soon as possible. The lawyer will represent you in the property purchase transaction and ensure that your rights and interests as a buyer are protected and compliant with the law.

5. Signing the S&P Agreement

The developer will provide the formal Sale and Purchase Agreement (S&P) to the buyer's lawyer. Within three weeks of receiving S&P, the buyer needs to sign it.

For Singapore citizens or Permanent Residents (PRs), if you need to use the Central Provident Fund (CPF), the lawyer can contact the CPF Board on your behalf. You can request the lawyer to handle this when you visit the lawyer's office to submit the S&P.

If you are buying a house with a loan, you will receive a loan contract after the bank approves the loan, and you need to submit the loan contract to your lawyer's office. If you have any questions, the lawyer can explain the terms in the loan contract to you.

6. Paying Stamp Duty

Within two weeks from the execution date of signing the S&P, the corresponding stamp duty must be paid.

7. Completing the Transaction

Within eight weeks after signing the S&P, you need to pay 15% of the total purchase price as the down payment and complete the transaction procedures. The payment can be made in the form of a cheque to your lawyer's office, which will then forward it to the developer before the deadline.

8. Waiting for the Condominium to Be Completed (Building Under Construction Progressive Payment)

In Singapore, when purchasing a condominium under construction, homebuyers make payments in stages according to the progress of the project. For example, pay the first payment of 10% to the developer when the foundation is completed, and then pay the second payment of 10% to the developer when the building frame is completed, and so on.

During the waiting period for the delivery of the house, apart from the 20% (5% + 15%) of the payment already made, the remaining 80% of the house price will be paid in stages. Currently, the maximum loan is 75%, so the 5% for the foundation stage must be paid in cash or with CPF. After each progress of work is completed, the developer will send a letter to notify your lawyer to arrange for the buyer to pay the progressive payment. Depending on each person's payment plan, you can pay in cash or the bank will pay the corresponding loan amount. Correspondingly, the monthly mortgage payment for each progress will adjust accordingly - calculated according to the loan amount that the bank has already paid to the developer based on the progress of work. Therefore, compared with resale property, the financial pressure for new property is usually lighter.

When you receive the keys to the new house, you need to pay the 8th progressive payment of 25%. Usually, by this time, only 85% of the house price has been paid, and the final 15% balance will be paid when the Certificate of Statutory Completion (CSC) is obtained. Usually, this stage takes 6 - 12 months.

The following table is provided by the calculator of HouseBell, taking a new condo worth $2 million as an example, it outlines the progressive payments required at each stage of construction and their coressponding timeline,for reference only:

9. Property Inspection

New Project developers in Singapore will provide a one-year warranty period. Within 12 months after the property is handover, the developer is obliged to carry out free repairs for any defects found in the house, including household appliances and air conditioners. Therefore, the buyer should inspect the house carefully and promptly after taking possession. If any quality defects are found in the house, notify the developer in time for rectification.